Tax Consequences of Selling a Dental Practice: Simplified Guide to Considerations in IDSO Partnerships

Big Disclaimer: I am not a CPA or tax lawyer and not giving legal or tax advice! LPS clients are introduced to expert CPAs and tax lawyers which can help you understand the full tax implications of selling your dental practice in an IDSO partnership.

In the end, the net, after-tax proceeds in an Invisible Dental Support Organization (IDSO) partnership are really all that matters. What a doctor puts into their pocket at closing and after paying Uncle Sam and Governor Red or Blue in their state (41 of them) is what really counts.

In short, if negotiated correctly, the cash a doctor receives in purchase consideration for their practice will be taxed predominantly at long term capital gains tax rates of 20% Federal IRS. In this article, we will explore some of the potential tax consequences of selling a dental practice as well as a few factors to consider in an IDSO partnership.

State Taxes and Personal Domicile

Depending upon your personal domicile (not necessarily that state in which your practice is located, but where you “live” for tax purposes) you may also have a state income tax payment due to the state. LPS has more than a few client doctors whose practice is in a high tax state, but are actually legal residents of a no tax state.

The state taxes in some states are not nominal, and can be another 13.3% in California or 10.75% in New Jersey as examples. Or, you may luckily live in one of the nine states (Alaska, Florida, Nevada, New Hampshire, South Dakota, Tennessee, Texas, Washington and Wyoming) which have no capital gains taxes.

Dispelling Myths – Obama 3.8% Investment Tax

In addition, your CPA may claim that you owe the 3.8% Obama tax on your IDSO partnership transaction gains. If you are being told that by your CPA, you most likely need a new one. There are exemptions from this tax which most doctors qualify for when selling all or part of their practice.

Depreciation Recapture and Basis

And to make tax calculations even more challenging, you may have recapture requirements on depreciation which are unique to your tax situation. And your tax cost basis in the practice is critical to fully understanding your potential tax bill. This is why you hire a professional CPA or tax lawyer in the LPS process. We can guide you to the good ones.

Tax Allocation Negotiation in IDSO Partnerships

Like everything else in an IDSO partnership, the Tax Allocation is negotiable. Doctors who attempt transactions without a qualified advisor often neglect this very important piece of the net, after-tax value puzzle and therefore have much lower net proceeds.

In the sale of your dental practice to an IDSO, the documents and deal structure will include an agreed Tax Allocation. In summary, this is where the IDSO and the doctor negotiate what portion of the purchase consideration to allocate to goodwill and how much to the tangible assets being purchased. If your practice value at closing is $10,000,000, failing to “win” this negotiation can cost a doctor literally millions of dollars in unnecessary tax liability.

Doctors benefit by having a high component of the purchase price allocated to Goodwill. Whereas the IDSOs would prefer to have zero Goodwill and all of the purchase price allocated to tangible purchased assets.

Illustrative Examples of Tax Allocation Impact:

To grasp the significance of tax allocation negotiation, consider the following examples assuming $10,000,000 cash consideration:

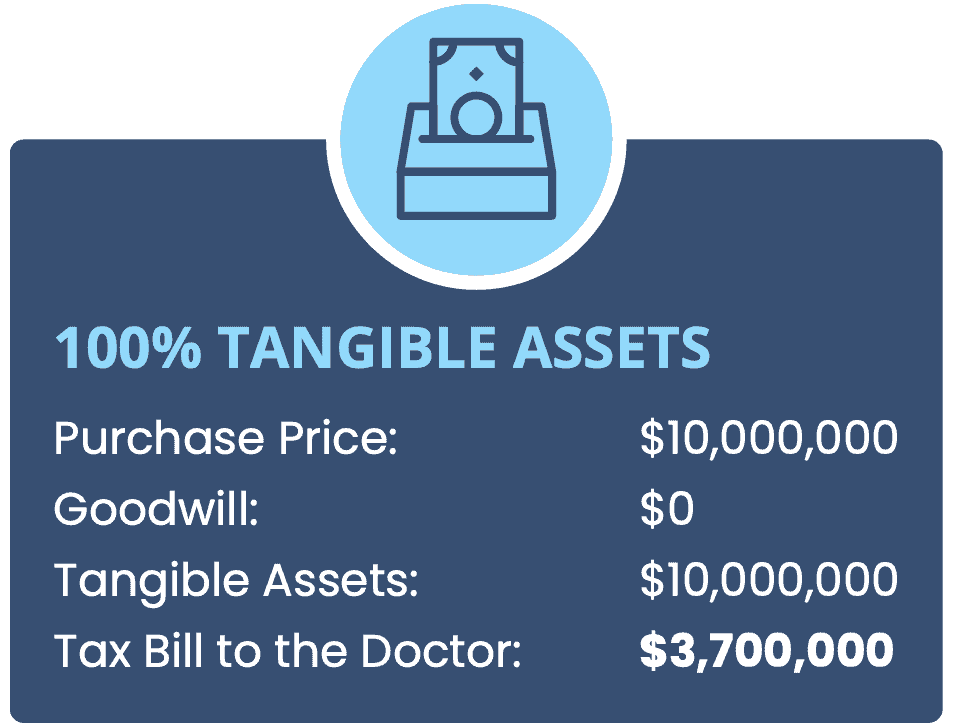

100% Tangible Assets

Purchase Price: $10,000,000

Goodwill: -0-

Tangible Assets: $10,000,000

Tax Bill to the Doctor, Federal Only: $3,700,000

100% Goodwill

Purchase Price: $10,000,000

Goodwill: $10,000,000

Tangible Assets: -0-

Tax Bill to the Doctor, Federal Only: $2,000,000

No transactions will end up in either scenario above, but we do see doctors who attempt these transactions, without LPS advice, end up with 50% Goodwill and 50% Tangible assets which results in a much higher tax bill than necessary.

Example:

Purchase Price: $10,000,000

Goodwill: $5,000,000

Tangible Assets: $5,000,000

Tax Bill to the Doctor, Federal Only: $2,850,000

In most cases, LPS has been able to win the tax allocation negotiation for the benefit of the doctor which results in a much lower tax bill. Example of an LPS negotiated tax allocation using 90% Goodwill.

Note: Our average negotiation has resulted in about 94% Goodwill in the last one billion dollars of practice transactions:

Purchase Price: $10,000,000

Goodwill: $9,000,000

Tangible Assets: $1,000,000

Tax Bill to the Doctor, Federal Only: $2,170,000

The key is to understand how to win this negotiation with hard numbers which the IDSO cannot dispute. This is where a competent advisor, like LPS, which is only paid by the doctor, not by both the doctor and the buyer, adds value. The tax savings we achieve for our clients alone can often offset the entire LPS fee.

When an advisor is paid on both sides of the transaction, they are less likely to advocate for the doctor’s sole interest. This is true in not only achieving the highest initial values with multiple bidders, but also in negotiating the complex terms of the partnership including the tax allocation. The conflicted little advisors literally result in lower values and less favorable deal structures.

Tax Treatment of the Retained Equity Portion of an IDSO Partnership

In most cases, the equity a doctor receives as a part of an IDSO transaction will be taxed at Long Term Capital Gains tax rates at the time they liquidate their ownership position in the future. Or in a few cases, doctors fearing higher tax rates in coming years will “prepay” this liability at today’s tax rates.

Bottom Line

The net, after tax cash you put in your pocket is dictated by the overall IDSO partnership structure, including all of the minutiae details. The headline 10x EBITDA sounds great at the country club bar, but how much you actually put in your pocket is all that counts.

Doctors will join an IDSO or compete with many!

At LPS, we specialize in helping doctors navigate the complexities of tax consequences in IDSO partnerships, ensuring optimal results. Join the ranks of successful doctors who have made informed decisions with LPS by their side and contact us today.

Recent Posts